For years, Indian investors have been told that “long-term investing” means picking a good fund and staying put. But as we approach the final years of a financial goal—like a child’s education or our own retirement—that “stay put” strategy can be dangerous. If the market crashes right when you need to withdraw the money, a decade of gains can vanish in weeks.

Yesterday, SEBI changed the rules of the game. They introduced a brand-new category: Life Cycle Mutual Funds. In this first deep-dive for Arthveda, we break down what this means for your wallet and why your old “Solution-Oriented” funds are being phased out.

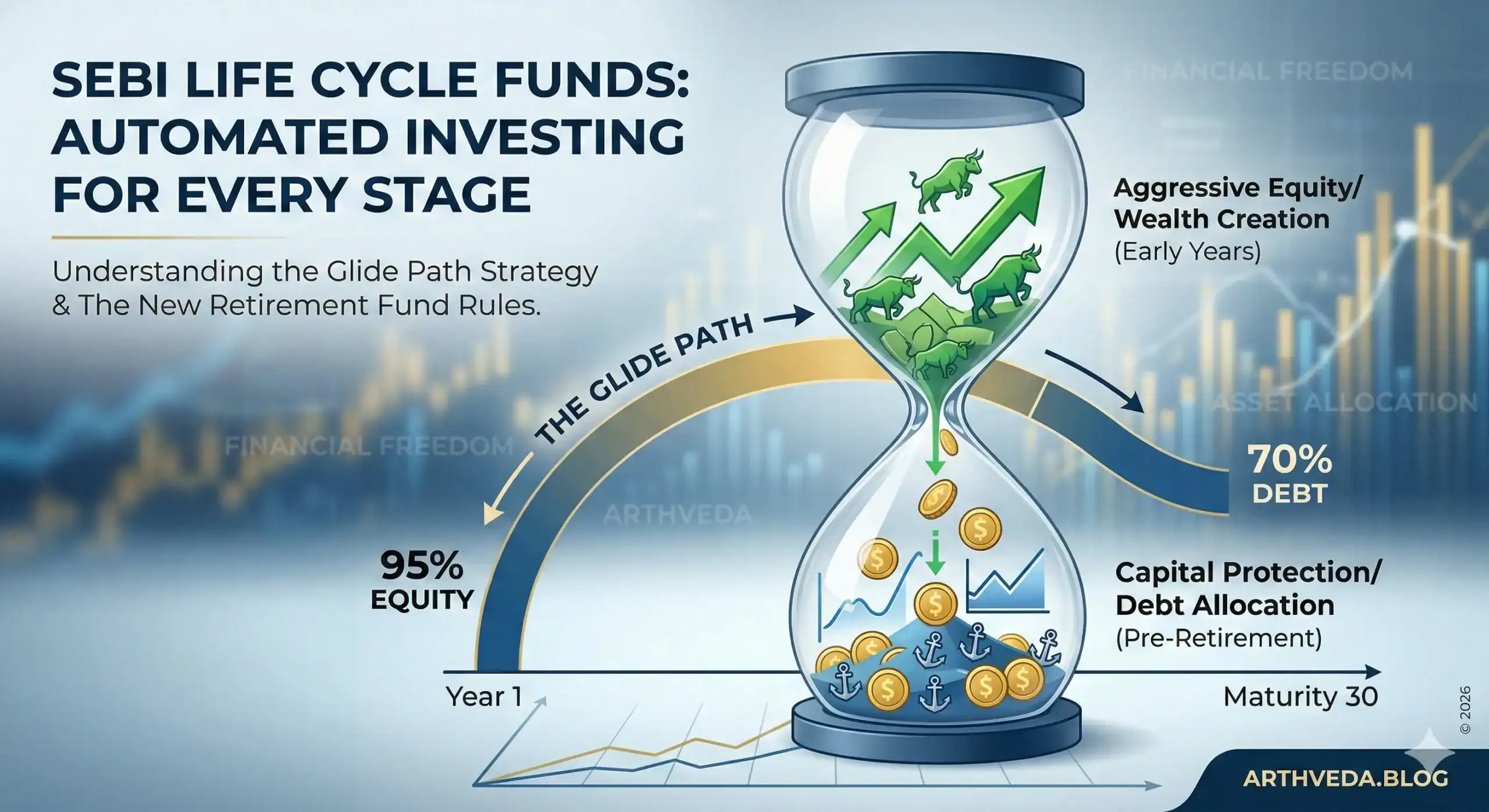

What exactly are Life Cycle Mutual Funds?

Imagine a pilot landing a plane. When the destination is 500 miles away, the plane flies high and fast to cover distance efficiently. As it nears the runway, it doesn’t just “stay put”—it slows down, lowers its altitude, and prepares for a safe landing.

A Life Cycle Mutual Funds works exactly like that. It is an open-ended scheme with a predetermined maturity date (e.g., Life Cycle Mutual Fund 2045) and a sophisticated “Glide Path” strategy.

- The Early Years: When the maturity date is 15–30 years away, the fund invests heavily in Equity (65%–95%) to grow your wealth aggressively.

- The Transition: As the years pass, the fund automatically “glides” into safer territory.

- The Landing: In the final year before maturity, the equity exposure drops significantly (5%–20%), while Debt (up to 65%) and safer assets like Gold or Silver ETFs take over to protect your accumulated corpus.

The End of “Marketing Gimmicks”: Solution-Oriented Funds Scrapped

The most shocking part of the SEBI circular was the immediate discontinuation of the “Solution-Oriented” category. For years, AMCs sold “Retirement Funds” and “Children’s Gift Funds” that were often just regular hybrid funds with a fancy name and a lock-in period.

Under the new 2026 rules:

- No New Subscriptions: Existing Retirement and Children’s funds have stopped taking new money as of February 26.

- Mandatory Mergers: These older funds will be merged into Life Cycle Mutual Funds or other diversified schemes that match their actual risk profile.

- True-to-Label: SEBI is banning “return-emphasizing” words like “Wealth Creator” or “High Growth” in these names. If a fund is meant for a 2050 goal, it must be named Life Cycle Mutual Funds 2050.

Key Technical Features of the 2026 Framework

If you are planning to switch to Life Cycle Mutual Funds, you need to understand the structural guardrails SEBI has put in place to protect you:

| Feature | Detailed Regulation |

| Tenure | Available in multiples of 5 years (Minimum 5 years, Maximum 30 years). |

| Asset Classes | A multi-asset mix including Equity, Debt, Gold/Silver ETFs, and InvITs. |

| Debt Quality | Debt holdings must be AA or higher-rated and mature before the fund does. |

| AMC Limits | A single fund house can only have a maximum of 6 such funds active at once. |

| Maturity Mergers | Funds with <1 year left can be merged with the next nearest maturity fund. |

The “Discipline” Tax: Understanding Exit Loads

To ensure investors don’t treat Life Cycle Mutual Funds as short-term trading vehicles, SEBI has mandated a high, staggered exit load structure. This is designed to “inculcate financial discipline”:

- 3% Exit Load if you withdraw in Year 1.

- 2% Exit Load if you withdraw in Year 2.

- 1% Exit Load if you withdraw in Year 3.

At Arthveda, we view this as a “protection tax.” It keeps the fund stable and prevents the fund manager from having to sell stocks during market panics just to pay out flighty investors.

Why Every Investor Needs a “Glide Path”

The biggest challenge in retail investing isn’t picking the right stock; it’s the Sequence of Returns Risk. If you have a ₹1 Crore corpus for your daughter’s marriage and the market drops 40% in the final year, you are left with ₹60 Lakhs.

Life Cycle Mutual Funds solve this by removing human emotion. The “Glide Path” is a mathematical schedule. As the time to your goal reduces, the risk reduces automatically.

The Arthveda Verdict: Should You Invest?

The Life Cycle Mutual Funds category is a massive upgrade for “set-and-forget” investors.

- Who it’s for: Parents planning for education, professionals building a retirement nest egg, and anyone who finds manual rebalancing stressful or tax-inefficient.

- Who it’s NOT for: Tactical investors who like to time the market or those who want absolute control over their asset allocation every month.

Our Take: For 90% of Indian families, Life Cycle Mutual Funds are the most practical way to reach a long-term goal. They offer a tax-efficient way to rebalance (as switching between separate Equity and Debt funds triggers capital gains tax, whereas internal rebalancing within a single fund usually does not).

What You Should Do Today

- Audit Your Portfolio: Check if you own any “Retirement” or “Children” branded funds. Look for communications from your AMC about upcoming mergers.

- Identify Your Target Year: Do you need money in 2035? 2045? 2055? Align your future SIPs with a Life Cycle Mutual Fund that matches that specific year.

- Stay Disciplined: Don’t let the 3% exit load scare you—use it as a reason to stay committed to your 20-year vision

The introduction of Life Cycle Mutual Funds marks the end of “emotion-based” selling and the beginning of “time-based” investing in India. At Arthveda, we believe this is the safest way to ensure your financial plane lands exactly when and where you need it to.

SEBI’s New Rules: Life Cycle Funds vs Retirement Funds

This video explains the recent SEBI shake-up where solution-oriented categories were scrapped in favor of the more structured life cycle fund model.

The Ultimate Guide to Mutual Funds: Invest Smart, Grow Wealth