The New Income Tax Act 2026 is designed to eliminate archaic language and redundant provisions. One of the most significant structural changes is the removal of the confusing “Assessment Year” and “Previous Year” terminology, replacing them with a single, unified “Tax Year.” For salaried individuals and MSMEs, the focus has shifted toward a simplified, exemption-free regime that rewards higher take-home pay while significantly reducing the litigation burden. In this report, we deconstruct the new slabs and the strategic maneuvers required to optimize your tax outgo.

1. The 2026 Tax Slabs: Who Wins?

The Union Budget 2026 has doubled down on the New Tax Regime as the default choice. Under the New Income Tax Act 2026, the exemption limits have been aggressively expanded to provide relief to the middle and upper-middle-income groups.

| Taxable Income (₹) | New Tax Rate (2026-27) |

| 0 – 4,00,000 | Nil |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| 16,00,001 – 20,00,000 | 20% |

| 20,00,001 – 24,00,000 | 25% |

| Above 24,00,000 | 30% |

The “Zero-Tax” Threshold

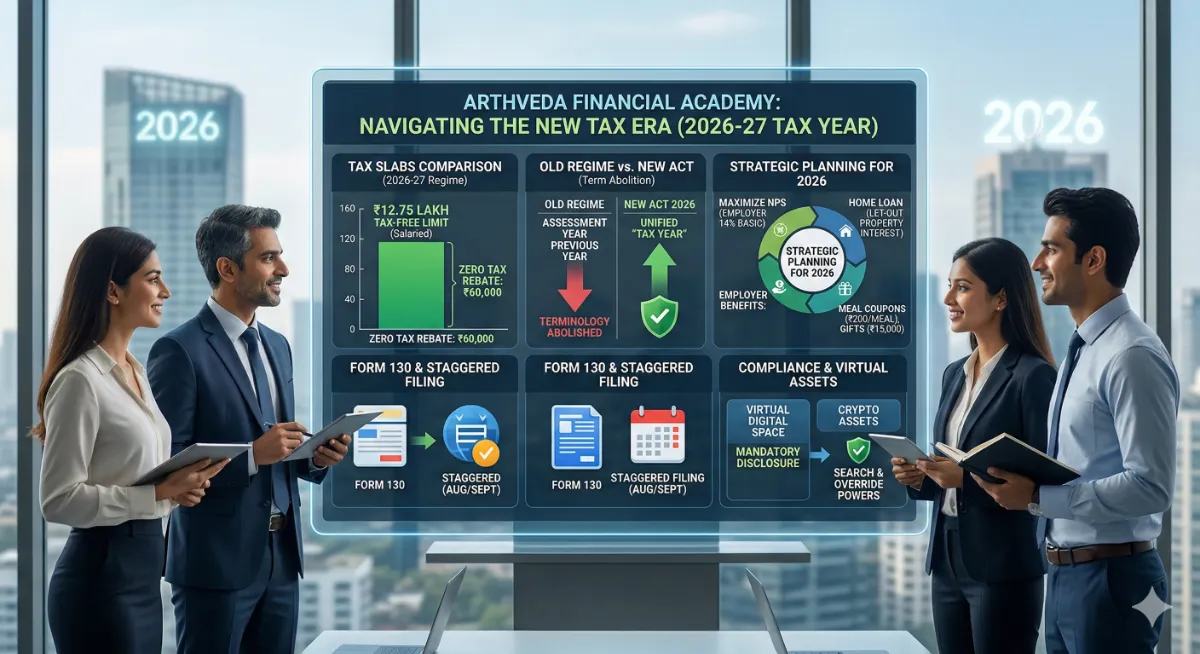

A masterful update under the New Income Tax Act 2026 is the enhanced Section 87A rebate of ₹60,000. This ensures that resident individuals with a taxable income of up to ₹12 lakh pay zero tax. For salaried employees, adding the ₹75,000 standard deduction effectively makes an income of up to ₹12.75 lakh tax-free.

2. Strategic Tax Planning in the New Era

Tax planning under the New Income Tax Act 2026 is less about “investing to save” and more about “efficient asset allocation.” Since most 80C and 80D deductions are absent in the new regime, your strategy must pivot.

A. Maximizing Employer Benefits

The new rules have increased the exemption for free food and beverages from ₹50 to ₹200 per meal. Additionally, the perquisite value for employer-provided gifts is now exempt up to ₹15,000 (previously ₹5,000). Structuring your salary with these components is a masterful way to reduce your taxable base without affecting your cash flow.

B. The NPS Advantage (Section 80CCD(2))

Even in the new regime, the employer’s contribution to the National Pension System (NPS) remains a powerful tool. Under the New Income Tax Act 2026, this deduction is allowed up to 14% of basic pay, providing a significant shield for high-income earners.

C. Home Loan Strategy for Let-out Property

While interest on self-occupied property is not deductible in the new regime, the New Income Tax Act 2026 still allows the entire interest paid on a “let-out” (rented) property to be claimed against the rental income. This remains a key pillar for real estate investors.

3. Digital Enforcement and Virtual Assets

The New Income Tax Act 2026 introduces the concept of a “Virtual Digital Space,” encompassing everything from email servers to online trading accounts.

- Crypto Assets: It is now mandatory to furnish detailed information on all crypto-asset transactions.

- Enhanced Search Powers: Tax authorities now have explicitly defined powers to access electronic media and override access codes during searches if a taxpayer fails to cooperate.

4. Relief for Senior Citizens and Physically Challenged

The New Income Tax Act 2026 has shown significant empathy toward specific demographics:

- Senior Citizens: The deduction for interest income (80TTB) has been increased to ₹1 lakh, and the standard deduction for pensioners remains robust at ₹75,000.

- Physically Challenged Employees: The transport allowance exemption has seen a massive jump to ₹15,000 per month (plus dearness allowance) for those in metro cities.

5. Compliance Simplification: Form 130 and Staggered Filing

To reduce the last-minute rush in July, the New Income Tax Act 2026 introduces staggered filing dates. Furthermore, the old Form 16 has been replaced by Form 130, which is a more comprehensive, three-part certificate that includes specific annexures for senior citizens.

The ArthVeda Verdict

The New Income Tax Act 2026 represents a move toward a more “Trust-Based” governance model. While the loss of traditional 80C deductions might feel like a blow to those accustomed to the old regime, the significantly lower tax rates and the ₹12.75 lakh tax-free threshold offer a much higher disposable income for the middle class.

Your tax planning must now shift from “Tax-Saving” to “Wealth-Building.” Instead of locking money in a 5-year ELSS just for a deduction, you now have the freedom to invest in high-growth equities or liquid assets based on market merit, rather than tax coercion.

This video provides a professional breakdown of the transition to the new Act and how the decriminalization of offenses and simplified assessments benefit ordinary citizens.