Private Credit & Fractional Real Estate the investment landscape of 2026 is unrecognizable compared to a decade ago. Gone are the days when a “safe” portfolio meant a simple split between equity mutual funds and bank fixed deposits. As inflation remains persistent and global markets show increased sensitivity to geopolitical shifts, the traditional “60/40” portfolio is no longer sufficient. Enter the new frontier: Private Credit & Fractional Real Estate.

For the first time in Indian financial history, retail investors have been granted “VIP access” to asset classes that were once the exclusive playground of institutional giants and ultra-high-net-worth individuals (UHNIs). Through technological innovation and groundbreaking regulatory shifts like SEBI’s SM-REIT framework, you can now own a slice of a Grade-A office building or act as a lender to a high-growth startup with as little as ₹10,000.

The Democratization of High-Yield Assets

The core appeal of Private Credit & Fractional Real Estate lies in their ability to provide “alpha”—returns that exceed standard market benchmarks—without the extreme daily price volatility associated with the stock market. In 2026, “financial inclusion” has moved beyond just opening bank accounts; it is now about providing the middle class with the same wealth-building tools as the elite.

By diversifying into these private market instruments, investors are essentially moving away from “systemic risk.” When the Nifty 50 or Sensex dips due to global sentiment, your rental income from a commercial warehouse or the interest from a corporate loan continues to flow. This is the power of alternative investments.

Part 1: Deep Dive into Private Credit

Private Credit is the practice of non-bank institutions lending money directly to companies. In the Indian context, this has exploded because traditional banks have tightened their lending criteria, focusing primarily on home loans and large-scale infrastructure. This has created a massive opportunity for retail investors to step in as the lenders.

Why Private Credit is the 2026 Favorite

- Superior Yields: While a high-tier bank FD might offer 7.5% in 2026, private credit opportunities often range between 12% and 16% IRR.

- Asset-Backed Security: Most professional platforms ensure that these loans are “Senior Secured.” This means the loan is backed by company assets, and in the event of a liquidation, credit investors are the first to be repaid.

- Monthly Passive Income: Unlike stocks, where you wait for capital gains, private credit typically pays out interest on a monthly or quarterly basis, making it an excellent tool for cash-flow planning.

Understanding the Risk Profile

It is critical to remember that higher returns come with higher responsibility. The primary risks include:

- Default Risk: The chance that the borrowing company cannot pay back.

- Liquidity Risk: Unlike a stock you can sell in seconds, these are often “lock-in” products for 12–36 months.

Part 2: The Fractional Real Estate Revolution

For generations, the “Indian Dream” was to own property. However, buying a commercial office in a prime business district like BKC (Mumbai) or Cyber City (Gurugram) requires hundreds of crores. Fractional Real Estate solves this by allowing 100 investors to pool money and buy that asset together.

The 2026 Game-Changer: SM-REITs

The Securities and Exchange Board of India (SEBI) officially formalizing Small and Medium REITs (SM-REITs) has changed everything.

- Asset Size: Covers properties valued between ₹50 Crore and ₹500 Crore.

- Minimum Investment: Regulated platforms now offer entry points at ₹10 Lakh, while some unregulated (but popular) tokenization platforms go as low as ₹25,000.

- Governance: SM-REITs mandate that 90% of the net distributable cash flow must be paid out to investors.

Returns: More Than Just Rent

In 2026 Private Credit & Fractional Real Estate, commercial real estate yields are consistently beating residential. While a flat in Bangalore might yield 3% in rent, a fractional share in a tech park can deliver 8% to 10% rental yield plus an additional 4% to 6% in capital appreciation upon the sale of the asset.

Comparative Analysis: Top Platforms in India (2026)

To help you navigate this frontier, we have compiled a comparison of the leading players in the Private Credit & Fractional Real Estate space.

| Platform Type | Top Players (2026) | Asset Focus | Min. Investment | Expected Yield |

| Private Credit | Wint Wealth, Grip Invest | NCDs, Lease Finance | ₹10,000 – ₹1 Lakh | 11% – 15% |

| Fractional Real Estate | hBits, Strata, PropShare | Grade-A Offices | ₹10 Lakh (SM-REIT) | 8% – 12% (Rent) |

| New Age / Tokenized | ALT DRX | Luxury Villas, Units | ₹25,000 | 12% – 18% (Total) |

The 2026 Retail Investor’s Guide: Stepping into Private Credit & Fractional Real Estate

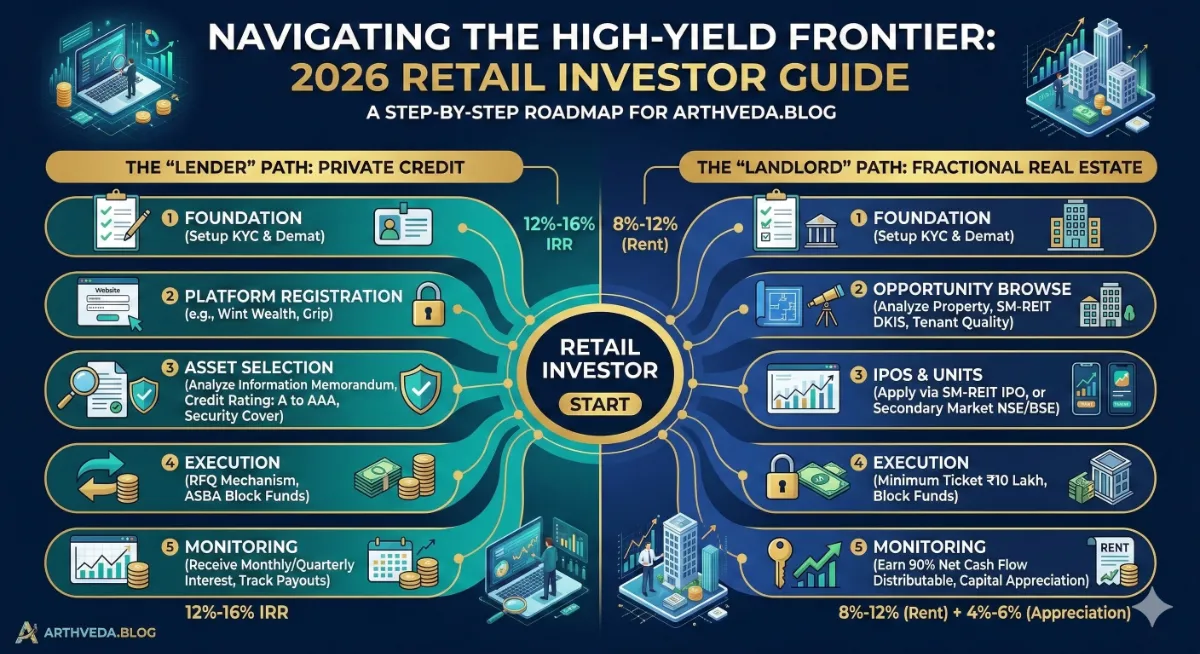

Phase 1: The Foundation (One-Time Setup)

Before you can invest in Private Credit & Fractional Real Estate, you must ensure your “Paperwork Infrastructure” is ready.

- Demat & Trading Account: For SM-REITs (Fractional Real Estate) and NCDs (Private Credit), you need a standard Demat account with brokers like Zerodha, Groww, or ICICI Direct.

- KYC Compliance: Ensure your KRA-KYC is “Validated.” In 2026, SEBI requires a seamless match between your PAN, Aadhaar, and Mobile number.

- Bank Linkage: Use a bank account with active ASBA (Application Supported by Blocked Amount) for IPOs or Net Banking for platform transfers.

Phase 2: Investing in Private Credit (The “Lender” Path)

Example Platforms: Wint Wealth, Grip Invest

- Step 1: Browse the Baskets. Log in to your chosen platform and look at available “Baskets” or individual NCDs (Non-Convertible Debentures).

- Step 2: Read the “Information Memorandum” (IM). Don’t skip this. Check the Credit Rating (Aim for A to AAA) and the Security Cover (How much collateral the company has pledged).

- Step 3: Execution via RFQ. When you click “Invest,” the platform uses the exchange’s Request for Quote (RFQ) mechanism. You transfer funds to the Clearing Corporation, and units are credited to your Demat within T+1 or T+2 days.

Phase 3: Investing in Fractional Real Estate (The “Landlord” Path)

Example Platforms: hBits, Strata, PropShare

- Step 1: The IPO Route. Most 2026 fractional deals are structured as SM-REIT IPOs. Search for the “Draft Key Information” (DKIS) on the platform or SEBI website.

- Step 2: Block Funds via ASBA. Just like a stock IPO, your money stays in your bank account but is “blocked” until the units are allotted. This ensures 100% safety.

- Step 3: Minimum Ticket Check. Remember, for regulated SM-REITs, the minimum entry is currently ₹10 Lakh. For unregulated tokenized property, it may be as low as ₹25,000.

- Step 4: Secondary Market Buying. If you miss the IPO, you can buy units directly on the BSE/NSE using your trading app.

Phase 4: Post-Investment Monitoring

Investing is only half the job. To be a successful “Arthveda Investor,” you must:

- Track Payouts: Private Credit pays monthly/quarterly interest. SM-REITs distribute 90% of rental income.

- Review Annual Reports: Every March, check the occupancy rates of the property or the default rates of the credit issuer.

- Tax Filing: Download your Capital Gains Statement from the platform to ensure you pay the correct 12.5% (LTCG) or slab rate (Interest).

Comparison Checklist for Your First Deal Private Credit & Fractional Real Estate

| Checkpoint | Private Credit | Fractional RE |

| Minimum Lock-in | 12 – 24 Months | 3 – 5 Years |

| Primary Risk | Borrower Default | Tenant Exit / Vacancy |

| Liquidity | Low (Hold to Maturity) | Moderate (Sell on Exchange) |

| Primary Return | Interest Income | Rental + Appreciation |

Tax Implications: What Stays in Your Pocket?

Taxation is where many investors lose their edge. In 2026 for Private Credit & Fractional Real Estate, the rules have been streamlined:

- Private Credit (NCDs): Interest is typically taxed at your marginal income tax slab rate.

- Fractional Real Estate (SM-REITs): Since these were reclassified as “equity-related instruments” in early 2026, Long-Term Capital Gains (LTCG) are taxed at 12.5% for gains exceeding ₹1.25 Lakh. This is a significant advantage over physical property which often suffers from high stamp duty and complex tax filings.

Building Your “Alternative” Portfolio

How much of your wealth should be in Private Credit & Fractional Real Estate? Professional advisors in 2026 suggest a “Satellite Strategy”:

- Core (70%): Equity Mutual Funds, EPF, and Liquid Assets.

- Satellite (30%): This is your high-yield engine. Split this equally between credit (for cash flow) and fractional property (for inflation-hedging).

The Verdict: Is it Right for You?

The combination of Private Credit & Fractional Real Estate represents the most significant shift in retail finance since the introduction of SIPs. However, it is not “set and forget” investing. It requires due diligence on the underlying asset and the platform’s track record.

If you are an investor who is tired of the 7% ceiling of traditional savings and has a 3-to-5-year horizon, the frontier is open. It’s time to stop just being a consumer of the economy and start being the (Private Credit & Fractional Real Estate) landlord and the lender.

Disclaimer: Investments in private markets and real estate carry risks. Always read the scheme documents and consult with a SEBI-registered advisor before investing.

Section 80C: Strategic Tax Planning & Investment Guide (2026)

Understanding SM-REITs and Fractional Ownership in 2026 Private Credit & Fractional Real Estate

This video provides an expert breakdown for NRIs and retail investors on Private Credit & Fractional Real Estate how to choose between FDs, REITs, and fractional deals, making it the perfect companion to your Private Credit & Fractional Real Estate step-by-step guide.

1 thought on “Private Credit & Fractional Real Estate: The New High-Yield Frontier”